-

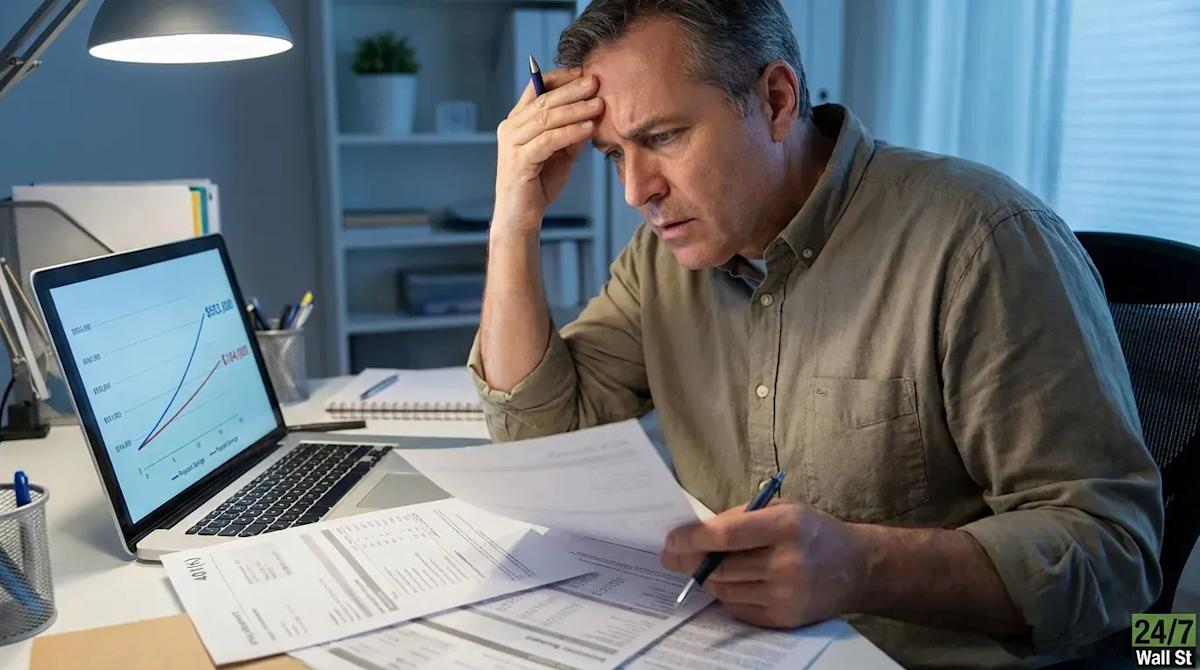

A 35-year-old who contributes 3% to a 401(k) accumulates about $184,000 by retirement, but if raised to 6% to get the full employer match, retirement savings will be closer to $553,000—a difference of hundreds of thousands of dollars from the single default that most workers never change.

-

Have you read New Report Changing Retirement Planning? Americans are answering three questions, with many realizing they can retire earlier than expected.

A 35-year-old on autopilot with a 3% enrollment rate would pay $1,950 a year and retire with about $184,000. That sounds like progress until you look at the amount that same person would accumulate by simply doubling his contribution rate to 6% and getting the full employer match: nearly $553,000. The difference, which amounts to hundreds of thousands of dollars, comes not from market timing or stock selection, but from a single default setting that most employees never revisit.

Plan sponsors intentionally set the auto-enrollment default low. The original logic was that low default rates would reduce the number of employees who would opt out for fear of reduced take-home pay. Three percent experienced no pain. The problem is that most people never revisit this number. Research consistently shows that inertia keeps most auto-enrollment participants at their default rates, sometimes for years or even decades.

According to 2025 data from Fidelity and Kiplinger, the most common employer match structure is a 50% match up to 6% of salary. On a salary of $65,000, contributing just 3% means losing half of your available employer match—about $975 per year. That forfeited money, if accumulated over the course of a career, could turn into tens of thousands of dollars in lost wealth. The employer match is the highest guaranteed return available to most workers, and default contribution rates result in millions missing out on it entirely.

Most plans include automatic contributions, automatic upgrades, and automatic enrollment. It increases your deferral rate by 1% each year until you reach a cap, which is usually 10% or 15%. According to Vanguard’s 2026 U.S. How to Save Preview, 71% of auto-enrollment plans include an auto-upgrade feature. However, the feature is almost universally opt-in, and most participants never activate it.

Have you read New Report Changing Retirement Planning? Americans are answering three questions as many realize they can retire earlier Better than expected.

A 35-year-old starting at 3% and increasing by 1% each year could reach a meaningful contribution rate in just a few years. The compounding effect of more than three decades of early rate hikes has resulted in a $200,000+ shortfall – not market timing, but simply keeping scheduled rate hikes in place. The damage is not from one bad year. This is due to a lack of contributions over the years during periods when compounding is at its greatest effect.

Still, 62% of automatic enrollment plans had delinquent employee contributions of at least 4% as of the end of 2025, still below the 6% threshold required to achieve a full employer match in most plans. For plan-eligible workers, even a 4% default rate would leave a sizable employer matching gap.

The SECURE 2.0 Act requires new 401(k) plans established after December 29, 2022 to automatically enroll at least 3% of eligible employees and automatically escalate by at least 1% each year until at least 10% is reached. But this authorization only applies to new plans, not existing ones. If your employer’s plan predates this, the old default settings still apply, and the upgrade feature may now be dormant in your account settings.

Consumer confidence data from the University of Michigan shows that as of January 2026, the consumer confidence index was 56.4, well below the neutral threshold of 80 points. Financial anxiety is high, which often prompts people to avoid looking at retirement accounts rather than participate in them. This is the environment where automatic registration defaults cause the most long-term damage.

The fix is not complicated but requires actually checking the account settings.

-

Check your current deferment rate. Workers who navigate to their 401(k) plan portal contribution settings and confirm their contribution percentage can determine whether they are leaving their employer’s money behind. Those who pay only 3% while their employer contributes up to 6% will lose free money every pay period. Increasing a $65,000 salary to 6% would cost roughly $1,950 more out of pocket each year, but an equal amount would be available from previously forfeited employer contributions.

-

Check out the automatic upgrade feature. It’s usually labeled “Auto-Increase” or “Contribution Upgrade” in the same settings screen. Workers set it at 1% growth per year, with the gap narrowing meaningfully over time. A 1% increase on a $65,000 salary is barely noticeable on most salaries. Most people never notice it.

Workers whose total household income is close to Medicare’s income-related premium thresholds may find that increasing their pretax 401(k) contributions also reduces their modified adjusted gross income, allowing them to retire without the impact of Medicare’s premium surcharge. This conversation is worth having with a fee-based advisor, but the starting point is confirming the current contribution rate.

You might think retirement is all about picking the best stocks or ETFs and saving as much as possible, but you’d be wrong. In the wake of new retirement income reports, wealthy Americans are rethinking their plans and realizing that even modest investment portfolios can become significant cash machines.

Many people even know they can retire earlier Better than expected.

If you are considering retirement or know someone who is, please take 5 minutes to learn more here.