-

Shift4 Payments shares have fallen over the past five years as investors lost interest in fintech.

-

The company is growing rapidly and generating free cash flow.

-

The valuation is cheap, and free cash flow is expected to roughly double over the next three years.

-

10 stocks we like better than Shift4 Payments ›

The new year is here, and all investors are trying to do the same thing: find the best stocks to buy and hold in 2026. This is a daunting task considering there are thousands of stocks to choose from. That’s why I like to narrow my search by focusing on industries that will be under pressure in 2025.

Investors are often wary of entire sectors of the stock market. When this happens, nearly every stock in the sector is punished. This can result in a good company being thrown out with the bathwater. That’s why I’m focusing on financial technology (fintech) today.

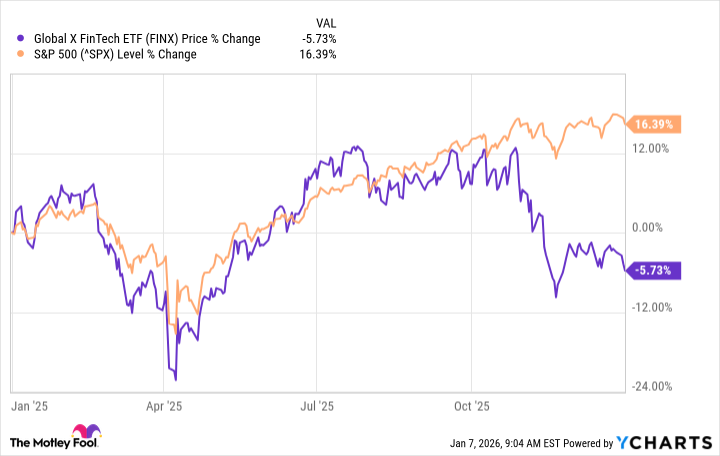

Fintech will lag significantly in 2025. To illustrate this, consider Global X Fintech ETF — an exchange-traded fund (ETF) focused on fintech stocks — and S&P 500 Index. As the chart below shows, the ETF has posted losses this year, in stark contrast to the market’s explosive gains.

The fintech industry has had a challenging year, which makes it possible that there may be a good opportunity for this hard-hit industry. i believe Shift4 payment (NYSE: IV) This is such a stock.

Shift4 provides payment processing hardware and software for hospitality venues, sports venues, restaurants and more. This isn’t entirely unique – many players in the industry do this. But Shift4 has grown substantially by focusing on high-volume customers, such as the aforementioned stadiums.

Few fintech companies have grown as fast as Shift4 in recent years. In the past five years alone, revenue has grown nearly 400%. Granted, its high-volume customer base tends to have lower profit margins, but that focus helps the business scale. Additionally, despite margin headwinds, management remains relentlessly focused on profitability, particularly free cash flow.

CEO Taylor Lauber said in a third-quarter letter to shareholders that Shift4 always prioritizes “where the next dollar is being spent as business free cash flow improves every quarter, and with urgency.”

As shown in the chart above, Shift4 has made continued progress in free cash flow, currently generating over $350 million annually. But its share price has stalled, meaning it now trades at a price to free cash flow valuation ratio of 16.

As of this writing, Shift4 shares are down 6% over the past five years, despite S&P 500 Index It’s up 85% – yikes! This is not what one would expect from a high-growth business.

Investors are unfavorable to the stock for a number of reasons. First, they worry about the industry as a whole. Competition is fierce and it is difficult to achieve long-term competitive advantage. The industry is facing disruption from cryptocurrencies, a risk that becomes more serious as crypto-friendly lawmakers take office.

Second, Shift4 made large-scale acquisitions, resulting in increased debt. In 2025, it acquired Global Blue, which handles tax refunds for overseas purchases, for $2.5 billion, a huge deal considering the company itself has a market capitalization of less than $6 billion.

The end result is that its debt has increased significantly in recent years. As you can see in the chart below, the company has high debt levels compared to its cash.

Shift4 is by no means in imminent danger, but its higher debt levels are concerning.

Investors may be worried about Shift4’s debt, but management isn’t. If it were concerned, it might focus some of its cash flow on reducing debt as quickly as possible. But management appears to be looking elsewhere.

At the end of the third quarter, management approved a $1 billion stock repurchase program and may be looking to make some big acquisitions quickly. During the quarterly earnings call, Lauber said he was “extremely pleased to be able to put capital into such a clear opportunity.”

In other words, Shift4 is authorized to reduce its share count by nearly 20%, and management may do so at short notice. This demonstrates management’s confidence in the strength of its business and debt sustainability.

However, the company may also believe that its stock price won’t stay low for long. Currently, the company is targeting an annual adjusted free cash flow run rate of $1 billion by the end of 2027. This implies free cash flow of at least $250 million in the fourth quarter of 2027.

Assuming Shift4 follows this path, its adjusted free cash flow would roughly double by the end of 2028. Valuations are already cheap. If it stays as cheap as it is now, the share price will double by 2028. Aggressive share buybacks will only further enhance its potential.

Shift4 stock was thrown out with the bathwater in 2025. But I suspect it will continue to underperform as we move into 2026.

Before buying Shift4 Payments stock, consider the following:

this Motley Fool Stock Advisor The analytics team has just identified what they believe is 10 Best Stocks Investors can buy now… and Shift4 Payments isn’t one of them. The 10 stocks selected could generate huge returns in the coming years.

consider when Netflix This list was created on December 17, 2004… If you invested $1,000 when we recommended, You will have $489,300!* or when NVIDIA This list was created on April 15, 2005… If you invested $1,000 when we recommended, You will have $1,159,283!*

Now, it’s worth noting stock advisor The overall average return is 974% — outperformed the market compared to the S&P 500’s 196%. Don’t miss the latest top 10 list, available via stock advisorand join an investment community built by individual investors for individual investors.

See 10 stocks »

*Stock Advisor returned on January 9, 2026.

Jon Quast works at Shift4 Payments. The Motley Fool has an interest in and recommends Shift4 Payments. The Motley Fool has a disclosure policy.

This explosive fintech stock could soar more than 100% by 2028. Originally posted by The Motley Fool