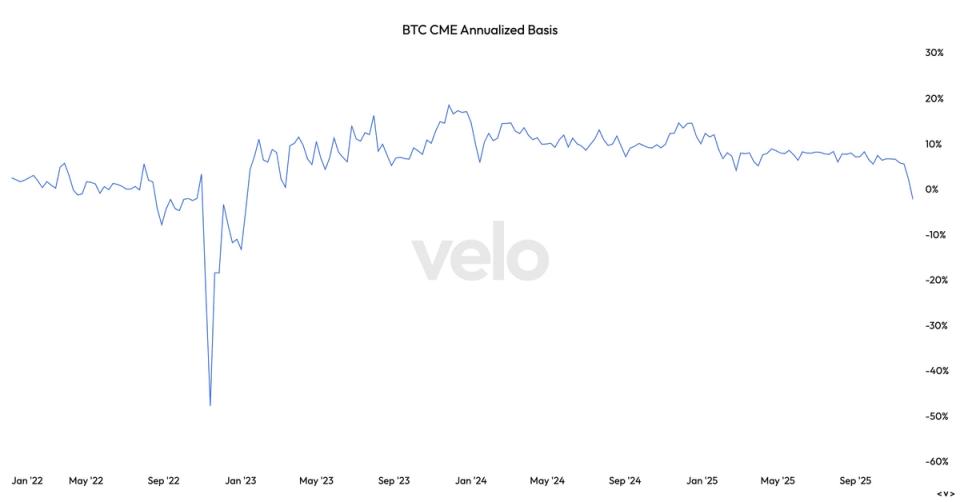

According to Velo data, the CME Bitcoin annualized basis has fallen to -2.35%, which is the deepest backwardation since the extreme chaos of the FTX crash in November 2022, when the basis was once close to -50%.

Backwardation describes a futures curve in which contracts expiring earlier trade at a higher price than contracts expiring later. In other words, the market will price Bitcoin in the future lower than its current or recent price. This creates a downward sloping futures curve and indicates that traders expect prices to weaken over time.

This structure is generally unusual in Bitcoin because Bitcoin futures almost always trade at a premium, called contango, reflecting the cost of leverage and the strong demand for forward risk.

The recent backwardation movement first occurred around November 19, just two days before Bitcoin bottomed around $80,000 on November 21. In the latest correction, a large amount of leverage was washed out of the system, traders liquidated long futures positions, and institutions reduced their exposure.

Historically, contango occurs at moments of pressure or forced de-risking, with previous events in November 2022, March 2023, August 2023 and now November 2025 closely correlated with major or local market lows.

However, backwardation does not automatically mean bullishness. As highlighted in earlier CoinDesk research, Bitcoin cannot compare to physical commodities such as oil, where backwardation reflects tight supply. CME futures are cash-settled, heavily used by institutions operating basis trades, and could slip further into negative territory.

In this view, backwardation represents cautious forward pricing and weaker expectations rather than strong near-term spot demand.

A significant portion of the leverage has evaporated, but the situation could always worsen if risk appetite deteriorates further. At the same time, this structure repeatedly marks a turning point once sellers are forced to exhaustion. As a result, Bitcoin is entering an area of historical danger and opportunity.